Kevin Warsh, the New Fed Chair Who Will Decide the Next Global Economy

If Kevin Warsh is approved to lead the Federal Reserve, there is hope for the U.S. to deliver a Golden Age under the Trump administration and serve its role as the heart of the global economy.

(Hanako Cho)

Speaking at the World Economic Forum in Davos, President Trump sent a pointed message to Jerome Powell, chairman of the Federal Reserve Board: lower interest rates. “Growth and low interest rates can and should be achieved simultaneously,” he declared.

Trump had settled on his successor to Powell: Kevin Warsh, a former member of the Federal Reserve Board of Governors, whose nomination was advanced by the man Trump most trusts to decode his economic instincts. Even the Wall Street Journal, which has grown increasingly critical of the Trump administration, praised Warsh as the best possible personnel choice during President Trump’s second term.

Unlike Chair Powell who is determined that economic growth triggers inflation, making interest rate hikes unavoidable, Warsh adheres to supply-side economics. Having left the Fed under Chair Ben Bernanke (who continued quantitative easing after the 2008 crisis), Warsh warned that such policies risk bringing about low growth and high inflation. His foresight has since been vindicated.

Dr. Arthur Laffer, the economist widely credited as the father of supply-side economics, recommended Warsh to President Trump. Dr. Laffer expressed high hopes about Warsh: “He will likely advance reforms through dialogue, much like President Reagan.”

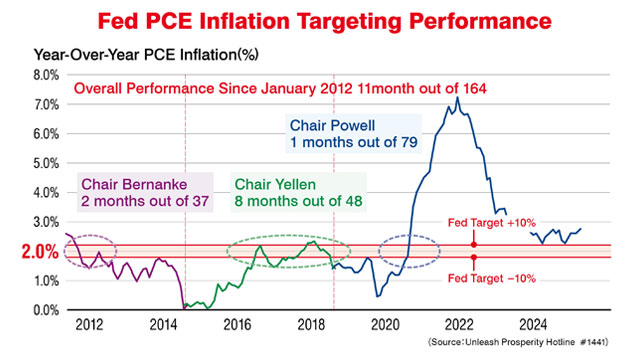

Chairman Powell Exported Inflation to the Rest of World

The fundamental issue is that Powell’s monetary policy did not merely fail the United States – it exported inflation to the world. Powell has consistently pursued policies aligned with the Biden administration.

For example, when former President Biden restricted domestic oil and gas production, causing energy prices to soar, or implemented pandemic relief payments between $3,000 and $4,000 per month that discouraged labor market participation, Powell failed to act. In August 2022, the Inflation Reduction Act was passed after being ridiculed as an “Inflation Acceleration Act.” Prices rose 21% under the Biden administration.

Amid growing concerns over inflation, Powell continued to make a claim that inflation was “temporary” and maintained expansionary monetary policy. Typically, monetary policy entails a significant time lag; as such, policy should have been formulated with a one-year forward-looking perspective. Instead, Chairman Powell fundamentally misjudged the surge in inflation and effectively exported that inflation to the rest of the world. It is difficult for him to escape the charge of having maintained a partisan bias toward the Democratic administration.

Furthermore, despite his failed predictions that the Trump tariffs would exacerbate inflation, he has faced no accountability. Such gross miscalculations by Chairman Powell are profound. As Dr. Laffer notes hereafter, the current structural problem of the Federal Reserve is that it uses its “independence” as a shield to avoid responsibility for its failures—a record of performance that, in the world of professional sports, would have called a forced retirement.

The Only Path Forward to Avoid Global Economic Crisis Is ‘Growth’

Why has this situation come about? The reason is that most of the Fed governors, except for some appointed by Trump, are Keynesian economists, clinging to the old demand-side model. This model is what Dr. Laffer explained with the apple analogy: “If apples are expensive, lower the demand for apples. Take away purchasing power from people through interest rate hikes.” Trying to slow down inflation by reducing total demand causes total production to decline and recession to arrive. That is, intentionally inflicting damage on the economy is the demand-side’s solution to fight off inflation. This model which contracts the economy is the opposite of Trump’s growth doctrine.

However, the model that is showing positive effects is supply-side economics. Under the Trump administration, GDP growth for the 3rd quarter of 2025 recorded 4.3%. Due to supply-side effects from Trump’s first-term large-scale tax cuts, total supply has increased, the growth rate has surpassed that of the eurozone, and household take-home pay has risen by more than $4,000 per year (approximately ¥600,000). Moreover, during the same period the inflation rate was suppressed to 1.9%. The same economic miracle as under the Reagan administration has occurred under Trump, who understands supply-side economics’ virtuous cycle.

If 3% growth continues, the government debt-to-GDP ratio will continue to decline, and after 30 years will approach near-zero, according to some calculations (see chart below).

Just as with Japan, America’s weak point is debt. If the U.S. economy falls into low growth and federal bond repayments are delayed, world interest rates will rise and financial instability will result. The world economy will be in crisis. To prevent that future, high economic growth rate must be sought at all costs. In this sense, not lowering lending interest rates is stifling economic growth, and in the long term will cause the dollar to lose credibility.

Coordination With Government Will Bring Economic Growth

Master Ryuho Okawa, founder of the Happy Science Group, has commented before on Japan’s stagnating economy: “If the Ministry of Finance and the Bank of Japan had not done strange things, and if the media had not propped up the wrong side, the Japanese economy would simply have doubled.”

The central bank’s coordination and cooperation with the government is indispensable for achieving a high economic growth rate; independence doesn’t mean to obstruct the government.

Moreover, President Trump states: “Our growth potential is infinite, and if we return to sound policy, it could grow even further.”

President Trump’s view on growth perfectly aligns with Warsh, who highly values the entrepreneurial spirit. Furthermore, President Trump is trying to make America like the “city upon a hill” as described in the Bible, that is, by creating a model nation for the world to lead global economic expansion. The arrival of a Golden Age is President Trump’s wish. The U.S. economy is the engine of the world economy.

The key players have lined up to solidify the foundation of 300 years of American prosperity: the next Fed chairman candidate Warsh, Treasury Secretary Scott Bessent, and National Economic Council Chairman Kevin Hassett all understand that economic growth must come first and are determinate supply-siders.

◆ ◆ ◆

An Interview With Dr. Arthur B. Laffer: Reforming the Fed

The Liberty spoke with Dr. Laffer regarding the direction of the economic reform that must be taken by the new Fed Chair. This interview was conducted on January 17th.

(Interviewer: Hanako Cho)

Returning to the Fed’s Original Roles: Regulate Banking and Create Price Stability

Dr. Laffer: What is the role of Fed chairman? Now, obviously, there’s been mission drift in the Fed. Whenever you get an organization like the Fed that’s independent, they start expanding their mission statement, and sooner or later, they have this massive mission statement that has nothing whatsoever to do with why they were put into place. And that is a classic problem of the Fed.

Just as an example of that, these are numbers I don’t know personally, but I’ve heard the numbers. There are about 300 PhD economists at the Fed. What’s that all about? They probably need 2. And that’s all they need, and probably not even those 2. You probably need someone who understands economics rather than has a PhD in economics.

It’s been this big breeding ground for economics, talking to each other, publishing to each other, doing all that, and wasting huge amounts of taxpayer money. And then, to the extent they do have any impact, it’s to make things worse. These economists are all sitting there in a government bureaucracy, and their whole role on Earth is to figure out ways of taking control of the economy away from the free enterprise system. And that’s one of the problems with the educational system in the U.S., probably everywhere. But the educational system is such that we train these people so much so that they think they should be able to control the world. And that’s the big mission drift.

The second issue, and if I can go back to the founding of the Fed in 1913, it had a price rule. The whole thing is to stabilize the value of the dollar and have a price rule. Now, in 1913, we had a gold standard for gold coins circulated freely within the U.S. Banks had their banknotes. Now, what the Fed did at that time, when it started to take over the monetary system of the U.S., was change the requirements for state banks versus federal banks. So, to issue notes, state banks would no longer use just state debt as their collateral. They had to use federal debt. And it became moving everything from state-run banks to federal banks. And that’s where the Fed came in. But it was a price rule, and they’re no longer on a price rule. They’re now under some sort of hand-waving system.

When you look at Powell and you look at the members of the Federal Reserve Board, it’s their opinion. They’re not trained. They don’t understand any of the stuff. Yet they have an opinion, “I think we should,” and that gets us into a lot of discussions later on that you’re talking about Stephen Miran and [President of the Federal Reserve Bank of Kansas City] Schmid, and which one’s right.

Should we cut it? Should we raise it? All that. And there should not be a difference of opinion. I mean, there should be a rule set there that what is the objective of the Fed, and the objective of the Fed should not be some sort of abstract, stupid rule like 2% inflation. Why 2% inflation? Why not 8% inflation? Why not 0%? I mean, you should have a stable currency, a stable value, and it should be stable from now and forevermore as far as we can tell. And I’ll go through some of that with you later, what it was like prior to the Fed.

Independence Without Accountability Creates an Irresponsible Fed

Dr. Laffer: Should the Fed be independent? And everyone says, “Of course, they should be independent.” And when you ask yourself that question abstractly, would you like to make sure that the people don’t make bad mistakes because they’re political? Of course, I would like to make sure that they make the right decision, whether it’s political or not. Everyone says that. But then the question comes is, what is it that incentivizes these people to make the right decision? Now, that’s the whole key there.

Let’s imagine we had two boards, one independent and one dependent. Now, how would you look at the two groups of people separately? Well, this one’s independent and can reject the administration, but it also can oppose the administration. It’s a bilateral thing. They can do bad things and good things, and they’re not held accountable. When you’ve got a Fed that’s controlled by the administration, you have an alignment of incentives, if, in fact, the Federal Reserve does do policies that raise inflation. If they’re independent, they aren’t fired. But if they’re part of the administration, they will be. The administration bears the consequences of Fed policies. And if, as long as it bears the consequences of Fed policies, they should have control over Fed policies.

If you’re going to be held accountable for your acts, you should be able to be responsible for your acts. You shouldn’t be blamed for someone else murdering someone, and someone else should not be blamed for you murdering someone else. To make the system work right, you need to associate responsibility with consequences. And in that sense, I believe clearly and completely that the Fed should be under the control of the administration. It should not be independent as it is now. And I have used the example with you many times of how the Defense Department should not be independent of the government. Health and Human Services should not be either, all of those are part of the central government.

Volcker’s Price Rule Is the Ideal Monetary Policy

Dr. Laffer: Now, what are the ways the central government controls monetary policy? That’s where we get into the price rule and quantity rule or just, “I think it should go up this week.” That’s where we go there. The Fed will be changed.

I’ve tried to get the objective function here is stop mission creep, reverse it, fire those 300 economists, get them out there. They’re doing nothing but harm. They need to be in the private sector. They don’t need to be sitting there planning how to control yours and my lives. Just get them gone. Reduce the mission statement and make it so it’s very, very tight. The role of the Fed is to regulate banking, yes, and to have price stability. That’s it.

Cho: That’s it.

Dr. Laffer: Nothing more. They’re not there to talk to bankers. They’re not there to give advice to presidents. That’s not their role. And you come back at this question a lot. What should they say? What should their comments be? They should just shut the hell up. Their job is to create price stability and make sure that banks are regulated in a way to have our monetary system function well. Period. That’s it.

And you can see their role on this. You can look at CPI. You can look at wholesale prices. You can look at spot commodity prices. You can look at interest rates. You can look at all of these numbers there. That is what they should focus on 100%. Period. Whether they’re independent or not, that should be their role. The Defense Department role should not be DEI. It should be defending America or carrying out the wishes of the president and the administration. So same thing is true with the Fed, okay? That’s where we are with them.

It Would Take at Least a Year to Make a Reform

Cho: Do you think the new Fed chair can implement these changes immediately?

Dr. Laffer: It takes a new Fed chairman, honestly, about a year to get really in control of the organization, the structure.

It takes a while to develop the relationships. Who’s your chief of staff? Do you replace your chief of staff? Who are the people that are important? Who’s not? What are the issues there? And what are the problems? You have no idea what the problems are when you look at this from the outside. But there are all sorts of private things going on in every organization as you know, and you need to get control of those. So don’t expect the Fed to change. Expect it to be a process. I would expect the new Fed chairman will be pretty much in control within six months to a year. So that’s just a natural part of any organization there.

So once that happens, now you say they come in in May, you’ve got maybe a nine-month period. In that nine-month period, we’re going to have midterm elections, both federal and state and local. So we’ll have a lot of other things in play. We’ll have to wait and see. In mid-January 2027, we will have a new House. We’ll have a lot of new senators. One-third of the Senate will be up for elections, so that could change things. We will have a lot of State House members. Every single State House member will be changed. We’ll have some state senators change. They’ll have some governors changed. So there’ll be a different construction of the U.S. political position there. I don’t know what it’s going to be, Hanako.

We have all sorts of things coming into this election. And depending upon the state of the economy, which I’m going to come back to you on – and I’m going to touch on the international, which I asked you about right away there – that will influence the elections. And if the administration keeps control of the House and the Senate and the State Houses and the governorships, that’ll be a very different political mandate than if the president and the administration loses control of much or all of those. That’ll be a different mandate as well and have very different consequences.

Lastly, the Supreme Court will not change. That’s one that will not. But that’s the only one that won’t.

What Dr. Laffer Considers to Be Noteworthy Policies Among OBBB

Dr. Laffer: When I look at the economy today – and let me just pull back and take a deep breath – Trump won the election in November, a year and a few months ago. He took office on January 20th, 2025. He’s been in office just about one year, not quite one year yet. If you look at all that’s been done in that year, it is breathtaking. It is shocking. We got the Big Beautiful Bill, which was—just barely passed. He was able to—this time, as opposed to 2017, when he came in the first time, he was able to really rein in the resources, rein in the troops, and have a much more concerted, focused effort rather than Republicans running all over the place, screaming, hollering, and Liz Cheneys and other—Kissingers and all that. Oh, just awful. This time, it’s very coordinated, very focused. It’s Donald Trump’s team.

The One Big Beautiful Bill did several things, and let me just go through them with you. It locked into stone, made permanent, all the tax cuts. Now, we had had a couple of them that were permanent. For example, the corporate tax rate of 21% had been made permanent by the 2017 Tax Cuts and Jobs Act. That was done. But there were others that had a 10-year horizon, and that would revert back. I think, really, one of the most important things that no one talks about is the reduction, dramatic reduction, in the death tax–

Cho: Yes, Death tax.

Dr. Laffer:–and the huge increase that would have occurred in the death tax had the Big Beautiful Bill not passed. That would have been really a bad thing. We also would have had a reversion of the personal income tax rate. He took the Tax Cuts and Jobs Act, took that from 39.6%, the top rate, down to 37%. If this had not passed, the Big Beautiful Bill had not passed, it would have popped back up to 39.6%. That would have happened. There would have been a bunch of other things, not only the death tax there, but it also made all of those permanent. It also introduced in the tax codes the 100% expensing of capital purchases. That is really a big deal, Hanako. I know it’s sort of niche-y and that type, but it is a big deal because if you have inflation, you have depreciation schedules that last over a number of years, the amount you depreciate the asset is far less than 100%. And it does change the internal rate of return on investments and does materially impact the capital labor ratio in the country, the investment ratios, all of that. Making 100% expensing is undervalued, and it’s really an important issue there.

You have several other things in the Tax Cuts and Jobs Act that– in the Big Beautiful Bill – excuse me – the Tax Cuts and Jobs Act, making that all permanent, it’s a big, big deal. In addition to that, they made no taxes on tips. It’s just common sense. Why would you spend a million dollars to collect a thousand dollars? And you’re going after tips. And I know all these people claim, “Well, it’s now automated.” It’s not true. Just stop already. Don’t try to catch people. A tax code should, in fact, be as voluntary as it possibly can be. The IRS should not be the enforcers. They should be the collectors of taxes that people voluntarily comply with and pay their taxes fair and square.

Yes, if someone’s a tax cheat, it is up to the IRS to find them out, get the money, and prosecute them. But that should not be their role. They should not be a hostile, nasty organization, and they have been. So, when you look at collecting taxes from a waiter or a waitress at a bar in Nevada, no, stop already. Just get rid of those. Where you have really, very great difficulties in collecting taxes, stop. Just don’t do it. And so, I love the no taxes on tips. I love the no taxes on overtime. I think that’s really one. It’s especially important in certain special circumstances. And let me stress this. If you work an extra hour or whatever it is, should you– I’m not really worried about that action. Whether you’re taxed or not, I’m not going to get up in arms and stomp around. I don’t mind it that you don’t have to pay taxes on your overtime.

But where I really want no taxes on overtime, where I really think it’s really, really important: firefighters in California who work 80 or 90 hours a week during a crisis. The people who come in and collect all the poisonous emissions from the train wreck in Palestine, Ohio, or for the 9/11 workers who come in when the attack was there, I want to make those people coming in on the big, big, big events. I don’t want to make them think twice because of the tax codes, and we’re going to tax the living hell out of you for working and saving people. That’s where I think the sale of this idea should be most prominent and where I think we should really tip our hats to these people who do work overtime to make America really do a great job.

And this is where you get– and you see what I’m saying. It’s when there’s a catastrophe in America, and we want everyone to work overtime, don’t tax the living hell out of them at higher rates and get it. That’s not what should be done.

And lastly, on the Big Beautiful Bill, I think are taxes on interest payments by car loans. Of course, that should be exempt. If you’re going to tax interest income, you should deduct interest expenses. We already do it with mortgage interest, and that’s right. So, I like what they did there. I like fair work. I like that they require work requirements for getting welfare. They didn’t do a lot of it, but they did require some. And there are a lot of other programs in there, school of choice, as in the Big Beautiful Bill– there are a lot of other things that I do like. I think the Big Beautiful Bill in its passage, which was narrow by both the House and the Senate and signed into law, is one of the most strikingly wonderful pieces of legislation the U.S. has done. It is taking care of all the department budgets well. It had them all folded into the One Big Beautiful Bill. It is just one magnificent piece of legislation. There are parts I could see improvements in, but we got it. We don’t need another one, Hanako. We’ve got that bill done.

If there were not a bill done in 2026, I’m not going to cry forever. If we lost the House– I would prefer us to keep the House, but if we lost the House, I’m not going to commit suicide. No Hara-kiri for me, okay? I said that to be Japanese a little bit, okay? I don’t think there’s any legislation this year that is a sine qua non, that is so important, “Oh my God, we’ll crash if we don’t do it.” I just don’t. That having been said, you see where I’m going on fiscal policy? I think we’re in really good shape. On government spending policy, which is also the Big Beautiful Bill, I don’t think we’re in good shape, but I think we’re in better shape than we were in 2025 and a lot better than we were in 2024, etc. We have a lot of distance to go still on government spending. DOGE, and you see all the stuff in Minnesota with the Somali crowd there and all the other things there. We need to go a lot further. That would be very helpful if we had control of the House to do that. But we’re in a lot better shape than we were before, but we could still improve a great deal. But if we lost the House, we won’t improve. But it’s not going to be me again jumping off the edge of a cliff.

Monetary policy, we’ve talked a great deal, you and I have over the years, and today on Kevin Warsh versus Kevin Hassett. Now, here I’m going to talk about what is the huge improvement that I’m hoping comes from Kevin Warsh, Kevin Hassett, and the other board members, and other members of the banks, the administration, the new Fed chairman, will have the ability to fire regional bank presidents. They will be there. So, it’s not like they have tenure and permanent thing, like Austan Goolsbee is head of the Chicago Fed. Now, he happens to be an exquisitely good economist. I’m quite a big fan of his economic research. I think he is very understanding, but there are some others that are not that are put in there because of DEI or because of political connections or whatever crap. So the Fed chairman will be able to replace these people right away.

And I think Kevin Hassett has a whole list of what he wants to do the day he takes office, if he does. And I would expect Kevin Warsh would too, but I haven’t talked to Kevin about that, Warsh. I have talked about it with Hassett. Hassett’s really well prepared to do a good job right away. What do they need to do? Well, we talked about the mission statement, mission creep. Stop all that. I’m not going to talk about those.

What the Fed Needs to Do Is The “Price Rule”

Dr. Laffer: Let me just talk about monetary policy because you focus on should they raise rates, should they lower rates, who does this, why would they? They shouldn’t be worried about rates. Period.

Cho: Why do you think that way?

Dr. Laffer: They should worry about the monetary base or the Fed balance sheet. They shouldn’t worry about what rates are in the market. Market rates should be determined by borrowers and lenders. It’s not by government officials who don’t know what they’re doing.

And Powell really doesn’t know what he’s doing. He’s a very nice man. I mean, you can see he’s a very gentle, nice man, but he doesn’t know what he’s doing. He should not be in the business of determining what rates are. He doesn’t know. He doesn’t understand. What we need to do is set a price rule. And I’m going to go through this with you carefully. Again, we’ve gone through it, you and I have a number of times, but let me set the price rule. What they need to do is set a set of policies that most likely give you stable prices, not 2% growth, stable prices, so you and I and everyone else can be very comfortable as to what the value of a dollar is going to be a year from now, 2 years from now, 10 years from now, 20 years from now, so we can make contracts in dollars. I would like to lend you a million dollars, and you pay me– over a 10-year period, you pay me back at 5%. And I know that as you pay me back, those dollars that you’re paying me back will be worth approximately the same thing they are today. That’s what you really want as a price. You have a price objective, which what you want to do is see a stable price, a stable value dollar, not an unhinged paper currency, not a 2% inflation rate and not a 10% inflation rate, not a minus 5%. You need to have it stable.

Now, whether it’s in the CPI or in labor wages, those we can discuss at length. But we want to have stable prices. Okay, you with me? To get stable prices, the Fed needs to control the rate of inflation, not the interest rate, not the balance sheet– not the balance sheet. So when the Fed looks at this, what they have to do is say, “Given what’s going on today, all right, what do you expect will be the consequence with regard to inflation in the future?” Now, when the Fed looks at things today, and you ask yourself, “What are lawyers’ wages, salaries today?” I don’t know. What’s the value of this, that or– most things, you don’t know what the price of that thing is, and you won’t know it until the prices come in six months from now, nine months from now, when we measure them, all right. All right? We don’t know. But what we do know with perfect certainty is what happens to spot commodity prices.

I know what the price of a board foot of wood is today. I know what the price of a tomato is today. I know what the price of gold is today. I know what the price– there are a lot of spot commodity prices that we know the price. If you stabilize spot commodity prices for the long, long term, sooner or later, the price of everything else is going to come into alignment with those spot commodity prices. This is the whole way the gold standard worked: if you fix the price of gold, sooner or later, the price level will adjust to that and will become stable, okay? So that is what the Fed needs to do. This is called the price rule.

Now, what does the Fed do? The Fed looks at spot commodity prices today and says, “Are they too high? Are they too low? Are they rising? Are they falling?” And when you look at this spot commodity prices, you need to look at them in the context of the economy. For example, if the economy is expanding rapidly, spot commodity prices tend to rise relative to all other prices. If the economy is contracting, cyclically contracting, they tend to fall much more rapidly than all other prices. They’re a highly volatile price measure. So when you look at stabilizing spot commodity prices, you need to take into account the state of the economy. So looking at spot commodity prices in the context of the economy, you ask yourself the question, “Are they rising too rapidly? Are they rising too slowly? Are they falling too rapidly? Are they falling too slowly?” okay, in the context.

And then what you say is, “If they’re rising too rapidly, I want to lean against that rise and–” so I would sell bonds in the open market. I would reduce the Fed’s balance sheet to make money scarcer, make the balance sheet scarcer, make the monetary base scarcer, so it tends to stop the rise in spot commodity prices. I pull money out of the system to make it so that those spot commodity prices rise at a slower rate than they otherwise would have, and I’ll keep doing that until I find spot commodity prices are no longer rising too rapidly, and we’ve got those increases under control. If spot commodity prices are falling too rapidly, if the deflation is not what you want for stable prices long term, what you then want to do is you want to buy bonds in the open market and expand the monetary base, the Fed’s balance sheet. You want to do it delicately, I think, until those prices no longer are falling too rapidly, and they’re now stabilizing.

And what the Fed needs to do, and what the Bank of England did on a three-times-a-day basis, is they looked at the markets and said, “Are the markets a little bit too inflationary today, in spot commodity prices a little bit less than–” and make minor adjustments on a monetary base. But the way you adjust the system is by looking at the balance sheet of the Fed, the monetary base, and you use interventions into the spot market there to re-stabilize the long-term spot commodity price index, which will, in turn, stabilize the overall price level. That is the price rule. Now, I’ve described that to you pretty technically here. I wrote this piece–

Cho: That’s what Paul Volcker did.

Dr. Laffer: Right. That is what Volcker did. If you go back, I wrote a piece in the Wall Street Journal with Chuck Kadlec (*), who worked for me on my conversation with Paul Volcker and how he understood the price rule. It is a personal gold standard, and it reinstates the hinged nature of a currency. The last thing you want is an unhinged paper currency. You want the paper currency hinged to goods and services so that you get stability. That is exactly what the gold standard was. And that is what Paul Volcker did to reinstate a modern commodity standard. And you can go and look at my piece in the Wall Street Journal in 1982 and see it. That is what we need to come back to if we are going to keep a Federal Reserve and government control over money. I’m not sure we need to do that. But that’s a much bigger question, which I’ll come to you in a minute.

Dr. Laffer: But that’s where I feel very comfortable that Kevin Hassett and Kevin Warsh both understand what I just described to you, how you technically implement it. That requires green eyeshades in there, but that’s a very important thing, implementing it correctly, getting rid of mission creep by the Fed and the independence. They need to stabilize prices. That they do. That should be every administration. What President Trump wants is lower interest rates, lower inflation. He wants that badly. A good Fed chairman should be able to give it to him. And I think Kevin Warsh and Kevin Hassett understand what I just described to you, Hanako.

Prior to 1913, The Government Had three Appropriate Roles

Cho: Before the Fed was established in 1913, what functions did the government perform with regards to Monetary Policy?

Dr. Laffer: And I hope you do understand it. Let me go back now — I’m going to pull back with you and go to the even bigger picture than this. We have a Fed. It became the first sort of incursion into the private money system that the U.S. had had. And I’m going to go through this again and forgive me for boring you. Prior to 1913, we had a private money system. We did not have government money. The government did three things prior to 1913. All three things were proper. They defined what a dollar was. A dollar is one-twentieth of an ounce of gold. That’s what it is. A dollar is one ounce of silver. That’s what it is. That’s the definition of a dollar. And that really makes a lot of difference when you analyze history. And maybe next time, we’ll go through that. But that’s number one. They defined what a dollar was.

Number two, they also minted gold coins and silver coins. If you came into the U.S. Mint, they would get a specie that you brought in, and they would then purify it to the right amount, okay? And then they would mint the coins. So you had silver dollars and gold, $20 gold pieces, $10 gold pieces, all that. You would have all of that, and they would charge you a commission for doing this. So you’d bring in your currency, your gold and silver, and they would do that. There were lots of private institutions that did the same thing, okay? Now, the government also told– it told the member banks that issued money, they had a form that they were supposed to issue. It would be a banknote from, let’s say, LaSalle National Bank or Citicorp or First Chicago or whatever, Wells Fargo. They would have a note that would be a banknote that would be a liability of the bank, not of the federal government. But they asked that they make them all into the same form.

So this is a banknote liable of First Chicago. And so they all look– but you could check and say, “It’s First Chicago. It’s not Citicorp. It’s not Wells Fargo.” And sometimes those banknotes sold at slight discounts or a premium to the other ones because the banks were a little bit more sound than other ones but not much. But you had this form so that everyone didn’t have– someone had pink things that went long. There was a structure like coins. The coins were all minted with a certain form, shape. Isaac Newton was a Master of the Mint back in the 16th, I think, and 17th century. And what he did was– you notice how coins all have those little perforations on the side? He was the one who put that in so you couldn’t take a gold coin and shave it with a knife and make it. So you could tell if that coin had been shaved or had not, so people would– just cool things like that story.

But these were all a private banking system. Banks had issued liabilities, checking accounts. They had banknotes, and they also had reported their financial statements. They had their balance sheets. They had their income statement. And the third role of government, prior to 1913, was to audit the banks to make sure that they were telling the truth, that if they said, “We had such and such as a reserve,” they went in and looked at them, “How much gold coins? What are your loans?” They did all of that to give you a good sense that they are reporting their financial numbers correctly, that they’re not fraudulent. So the government did define what a dollar was. It minted coins and regulated the format. And three, it audited the bank balance sheets. Those are the three functions.

Now, I say that. There were some exceptions prior to 1913. For example, from 1861 to 1878, because of the Civil War, we had a greenback period. So we had two currencies circulating. One was gold and silver, and one was dollar bills issued by the federal government. They did it for 1861 to 1878. By 1878, they retired all those greenbacks, and it went back to the way it was before. There were a couple of exceptions in there, and I’m not going to dwell on those with you.

From 1776 to 1913: The Inflation Rate Was 0% and the U.S. Became the Preeminent Economic Force on Earth

But from 1776 until 1913 – that’s 137 years – we had a private banking system. Over that whole period, the rate of inflation was 0%. It worked beautifully. Now, we did have some financial panics and crises, but not caused by money. There were panics that were caused by whatever things that happened. But we had none of those. We had a long-bond market. Now, this is by Jeremy Siegel and Jeremy Schwartz, who do the data.

Jeremy Siegel was a colleague of mine at the University of Chicago, probably the best data person on financial instruments there. From 1776 to 1913 long bonds were about 5.5% yield, and they went down to maybe a 4.5% yield over a century and a third. All right. Very stable. None of that. The system really worked well. There were financial panics, but there were no depressions, no crashes, no nothing. And during that period, the U.S. became the preeminent economic force on planet Earth.

Starting in 1913, as we’ve just discussed, they started taking over the Fed. Then we had Roosevelt declare gold illegal and he confiscated all the gold and then raised the price of gold, the biggest wealth tax in America. We were the only country that prohibited private holdings of gold with criminal penalties. And then the interest equalization, tax, the Voluntary Foreign Credit Restraint program, all of these other ones. And I was in the White House. I did my dissertation on this at Stanford. I was in there in 1972 when we went off gold. We became officially an unhinged paper currency as we are today.

And if you look at the period 1913 to the present, which is 112 years, something like that, the price level has gone up 32-fold. I mean, the dollar today is worth about 1% of what it was worth in 1913. And look at the price of gold, 4,500. Look at the price back then, it was $20 an ounce, now $4,500 an ounce. I could go through there. We’ve had major depressions, major crashes, panics, all of that stuff. Interest rates have been highly volatile. When we took office on January 20th, 1981, the prime interest rate in the U.S. was 21.5%. So, we have screwed up the monetary system incredibly by getting the government to nationalize and take over.

Shrink the Fed’s Balance Sheet

Dr. Laffer: The big picture, now, I’ve talked to you about the price rule, which given the government’s going to control money, you want a price rule. And in the bigger sense of the world, I would like to see the U.S. get out of the money market. There is no reason that the government should control money and should produce money and should be in any way, shape, or form involved in it. We had a period prior to 1913 where the government had no control of money. It was a private product, just like everything else, and it worked really well. Once they made it a public good, they’ve screwed it up really badly. I believe that the gold price and the emergence of cryptocurrencies, especially Bitcoin and Tether and some of these others, are the private sector’s response to a badly run monetary system and that the private sector is trying to create its own new money, and that that is the right way to go. But it’s a different level of question that you’ve asked on that.

So that’s where I would be on the long run, when you ask, “Should the Fed raise or lower interest rates?” They shouldn’t be in that business. When they raise interest rates or lower interest rates, the market doesn’t follow them. They should be fixing the balance sheet of the Fed if they do anything and slowly but surely running off those assets. They should get the balance sheet back down to maybe a trillion dollars. In 2008, I think the Fed balance sheet at the beginning of the Great Recession was about $900 billion. It went as high as $9 trillion. I don’t know where it is today. Maybe it’s $6.6 trillion, something like that. That balance sheet, the Fed should focus on a price rule and reducing that balance sheet back down to a trillion dollars-ish, much, much lower-level debt. And then they should use the Fed balance sheet to control using a price rule. That’s where they should go.

I think we’re going to move in the right direction with a new Fed chairman. I think it’s going to be a very positive thing for the market. But will we get to– will we get to a true price rule? I don’t know. Probably not locked in stone. If it’s a price rule, it probably will be run by the chairman of the board and by the Federal Reserve Board rather than by a rule or a law. I’d much rather see it done by a law. I’d much rather see that, but I’d much rather see us get rid of the money system entirely. But that’s not going to be in my lifetime there. So, I think I’ve covered pretty much what you want covered. I loved your questions, and I loved what you did. You’ve just done such a great job on this, and you’ve allowed me to just run with it.

Cho: Could you give me your opinion about whether the Fed chair should give any opinion about the government debt?

Dr. Laffer: I don’t think the Fed chair should be the person worried about debt or government debt. That should be the budget bureau. That should be all the departments and agencies. That’s the difference between tax rates, taxes, government spending, and mission creep of government in general, which is just outrageous. That’s where it should be. The Fed should be solely trying to stabilize the value of the dollar. And they should then try to bring their balance sheet down to a position where they’re at, let’s say, $1 trillion, which is plenty of balance sheet for them to be able to use that as a tool to stabilize the dollar. But I don’t like the idea of the Fed paying interest on deposits. And I don’t think they should worry about interest rates specifically. If they stabilize the value of the dollar, that’s all you need. Interest rates will no longer incorporate expected inflation, which is really what you want.

You do want interest rates to reflect the real rate of return on capital. You do want that. So if interest rates rise under a good price rule, that means that we’re having a real increase in real returns on capital, which just means that we’re having economic growth, and it’s great. And the expected real return on capital is ensconced in the 10-year bond yield and the 5-year bond yield and 1-year bond. So, I love it that interest rates are allowed to vary in the marketplace based upon the expected real return. What I want to see the Fed do is eliminate the expectations of inflation. And that is what they would do with a price rule. Let real returns be determined in the marketplace. You follow me?

Cho: Yes, thank you.

Dr. Laffer: I think that’s where we come out. The Fed has a very narrow thing. It’s really important, Hanako. Don’t, “Gee, it’s important.” But it’s not, should the Fed be concerned about an invasion of Venezuela? No. Should it be concerned about poppies growing in Iran? No. It should be stabilizing the value of the dollar – that’s its role – and regulating banks, making sure there aren’t bank cheats, financial cheats running around that stuff.

There are a lot of little nuances and little tricks and gimmicks and stuff and little– inside baseball that you don’t need to be aware of. Whenever you get inside the team, there are little things that happen. Should you use bonuses to Fed members who do a good job and penalize– should you worry about a bank collapse in California? Yeah. That’s where regulations should come in. Remember when we had Silicon Valley Bank collapse in California.

And they should be the lender of last resort and do all that. But that’s a different level of analysis. And that’s where you get to Walter Bagehot’s sort of how the Fed should run its daily operations. In times of crisis, discount freely but at high interest. So, you keep the system from collapsing. You provide liquidity to the system to make sure that something doesn’t go wrong. But that’s all short-term inside-baseball type of stuff. The long-term thing of the Fed is a price rule, and you should use the balance sheet intervention to do that. The exact opposite of what Powell and this team are doing. They lower interest rates by buying bonds in the open market, pushing up the price of bonds and lowering interest rates. The price rule way of lowering interest rates is to sell bonds in the market and to stop inflation. And by selling bonds and stopping inflation, bringing down the spot for money, you’re contracting the monetary. It’s the exact opposite. And it’s the exact opposite from Keynesian to supply side. We’re classical economists, and we’re right, and they’re wrong.

Cho: So, these 300 Keynesian economists are going to be fired.

Dr. Laffer: Yeah. Well, it’s also a good thing that they do because, frankly, they’re sitting there trying to get their reputations and getting hired and promoted by their publications. We don’t need any more economic publications. We need to reduce economic research by 90%. Most of the research is crap. I mean, just awful stuff. Get back to the way it used to be where the research was serious, and people read it, and everyone engaged in the debates. Not so you can get promoted to a local university. I did a paper in the newspaper. Spending $100,000 on an editorial in a newspaper is not worth it. It’s just not. And we need to get down to balance. One of the biggest overspendings in the U.S. is overspending on economists and on professors. And we have way too many professors, way too much research. We need to bring it back down.